The end of the student loan pause and rethinking repayment

The end of the federal student loan pause is drawing near (and the Supreme Court has spoken on loan forgiveness)—so, mark your calendars. In October, the student loan payment pause that began during the pandemic will end, and payment on $1.6 trillion in student debt will officially restart.

Physicians on average graduate with more than $250,000 in debt from medical school. And, with interest rates on the rise, monthly payments on that debt have only become more expensive.

Meanwhile, the weight of hefty student loans often triggers a “pay-it-off-at-all-costs” mindset among physicians. This is admirable, but such a rush to become debt-free can often overlook the nuances and potential opportunity costs of student loan repayment.

With the recent news on student loan payments, now may be a good time for many physicians to reset or rethink their approach to paying off student loan debt.

Understanding Public Service Loan Forgiveness (PSLF)

Firstly, let’s delve into the Public Service Loan Forgiveness (PSLF) program, which presents possibly a golden opportunity for physicians who work at non-profit hospitals.

The Public Service Loan Forgiveness (PSLF) program is a federal initiative that offers loan forgiveness to those working in eligible public service or non-profit roles. In essence, PSLF allows you to have the remaining balance of your loans forgiven after you’ve made 120 qualifying payments—that’s ten years’ worth—while working full-time for a qualifying employer. For many physicians, that employer is likely to be a non-profit hospital or a public healthcare facility.

This means that if you work for a decade in a non-profit hospital, the amount you owe after ten years, regardless of how large, could be completely forgiven under PSLF.

The strategy for those targeting PSLF is unique: It involves paying as little as possible during your repayment period. You might be wondering, “Isn’t the goal to pay off my loans?” Yes, under normal circumstances. But with PSLF, the less you pay, the more will be forgiven later.

So, how do you pay less? Most federal student loans have a 10-year term, so how do you even get to 20 to 25 years with a balance left? For that, you need an Income-Base Repayment (IBR) plan.

Choosing the Right Repayment Plan: PAYE or REPAYE

There are two main types of income-driven repayment plans: PAYE (Pay As You Earn) or REPAYE (Revised Pay As You Earn). Choosing which to go with is a vital piece of the puzzle. Each has its own eligibility criteria, benefits, and drawbacks. An informed decision, based on your income, marital status, and financial goals, can save you a significant sum in the long run.

If you need help, Core has teamed up with a trusted partner and financial advisor in GenFi, a company dedicated to helping physicians build wealth and manage their financial goals.

Pay As You Earn (PAYE)

PAYE caps your monthly student loan payments at 10% of your discretionary income. However, your payments will never exceed what you would have paid under the Standard Repayment Plan. This is beneficial for physicians who expect their income to rise significantly over time, as the cap can keep payments manageable.

Additionally, under PAYE, remaining loan balances are forgiven after 20 years of qualifying payments. Or, as mentioned above, for those working in the non-profit sector, loan balances may also be forgiven tax-free after 10 years under PSLF.

A significant advantage of PAYE is that if you’re married, you can file taxes separately from your spouse, and only your income (and not your spouse’s income) will be considered when determining your monthly payment.

Revised Pay As You Earn (REPAYE)

Like PAYE, REPAYE also caps your monthly payments at 10% of your discretionary income, but there is no cap on the payment amount as your income increases. This means that if your income rises significantly, so could your payments, potentially surpassing what you would have paid under the Standard Repayment Plan.

REPAYE offers loan forgiveness after 20 years for undergraduate loans and 25 years for graduate loans. However, unlike PAYE, if you’re married, your spouse’s income will be considered when calculating your monthly payments, regardless of how you file your taxes.

One unique feature of REPAYE is its interest subsidy. If your monthly payments don’t cover the interest accrued on your loans, the government will pay part or all of the leftover interest. This can significantly slow the growth of your loan if your income is low relative to your debt.

Regardless of which repayment method you choose, there is a catch.

The “Tax Bomb” Conundrum

Loan balances forgiven under PSLF are not considered taxable income by the IRS. However, the balances remaining on PAYE and REPAYE income-driven repayment plans are taxed as income.

Let’s look at a relatively standard hypothetical:

Dr. Smith graduates from medical school with a hefty student loan of $300,000, at an average interest rate of 6%. Many physicians choose to defer payments while in residency, which means when she finishes training she’ll owe $348,392 in accrued interest.

After residency, Dr. Smith enrolls in an income-driven repayment plan, specifically the PAYE (Pay As You Earn) plan. Dr. Smith’s starting salary is $200,000 and it increases 3% every year. She makes her payments diligently for 20 years.

Under PAYE, her payments cap at 10% of her discretionary income, which adjusts with her income over time. Despite making payments over two decades, the high-interest rate and her income-adjusted payments mean that she still has a remaining loan balance. In our example, after 20 years, she still owes $91,123.

This is where the “tax bomb” detonates. Under current tax law, the forgiven amount, in this case, $91k, is considered taxable income. If Dr. Smith is in the 24% tax bracket at the time of forgiveness, she could face a sudden tax bill of nearly $22,000.

A $22,000 tax bill is far less daunting than a $91,123 student loan. However, the key issue here is that the tax is due in one lump sum in the year the loan is forgiven. Careful planning to handle a potential tax bomb is essential.

The Role of Filing Status in Loan Repayment

Your tax filing status plays a significant role in determining your monthly payments under income-based repayment (IBR) plans.

If you’re married to another high-income earner, and you both file taxes jointly, both incomes will be taken into account when determining your monthly payments under IBR plans. This combined income could significantly increase your monthly payments.

However, if you’re on the PAYE, you can choose to file your taxes separately. This way, only your income is considered in the calculation of your monthly payments, which could keep your payments lower. The drawback is that you may lose out on certain tax benefits available to those filing jointly, such as certain credits and deductions. Therefore, it’s crucial to calculate whether the potential savings from lower monthly loan payments outweigh the lost tax benefits.

Meanwhile, if your spouse has little to no income, filing taxes jointly could actually lower your monthly payments. Under IBR plans, your payments are calculated based on your combined income and family size. Therefore, a lower combined income and larger family size could result in lower monthly payments.

Remember that under REPAYE, your spouse’s income is considered in your monthly payment calculation, regardless of your tax filing status. So even if you file taxes separately, your spouse’s income could increase your monthly payments.

The Question of Refinancing Student Loans

Another big question physicians often have is whether they should refinance long repayment periods into shorter ones in order to pay less in interest over time. Again, this goes to the “pay-it-off-at-all-costs” mindset.

Yes, if macroeconomic conditions are favorable, you could achieve a lower interest rate, which in turn translates into steeper monthly payments. Based on typical student loan balances for physicians, this could raise monthly payments in the realm of $4-6k/month. Steep indeed!

The problem many physicians run into is that life happens–a marriage, a new member of the family, perhaps a home purchase. Or an unforeseen financial emergency. Then the large, monthly student loan obligation could suddenly become a major stumbling block, impacting your ability to secure other loans or manage unexpected expenses.

Ultimately, you risk losing financial “optionality”—the ability to adapt your financial plans as life evolves. And that optionality itself could be incredibly valuable, preserving your ability to invest in other opportunities.

Let’s consider a hypothetical:

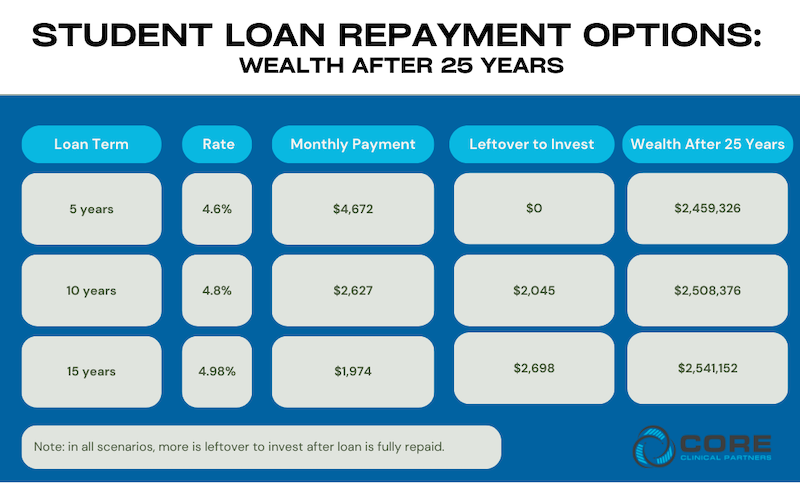

A recently graduated physician starts with a $250,000 student debt. The monthly payment varies depending on the loan term:

- 5 years: 4.6% interest = $4672/month

- 10 years: 4.8% interest = $2627/month

- 15 years: 4.98% interest = $1974/month

Let’s assure that the physician uses the savings in monthly cash flow from the 10- and 15-year term loans to invest, earning a fairly typical rate of return of 7%.

Here’s a table illustrating the total wealth at the end of 25 years under each loan term:

This table presents the total accumulated wealth at the end of a 25-year period, given the monthly investment that becomes available when opting for longer loan repayment terms. In this scenario, you end up $81,826 wealthier in the 15-year scenario as opposed to the 5-year.

The main point to note here is that even though it might seem tempting to pay off loans quickly, by doing so, one may potentially miss out on significant wealth accumulation through investments. In other words, there can be a substantial opportunity cost when focusing solely on quick loan repayment. As always, it’s essential to seek personalized advice from a financial advisor who understands your individual circumstances and financial goals.

The Trade-off Between Aggressive Repayment and Financial Flexibility

All of this doesn’t mean physicians need to abandon the idea of aggressive student loan repayment. Instead, we recommend a balanced, personalized approach, ideally in consultation with a financial advisor such as GenFi.

For example: consider keeping a longer loan term, but make payments as if it were a 5-year term. You will reap most of the benefits of a shorter term, such as paying less interest overall, but preserve your financial flexibility. If life throws a curveball, you have the option to reduce your payments back to the lower required amount.

Finally, we know there is a lot to think about here, and the pressure of student loan payments can be overwhelming. The drive to shake them off is powerful.

But as a physician, your financial journey is a marathon, not a sprint. Every decision, including student loan repayment, should be made with a holistic view of your financial health and goals.

Student loans shouldn’t be the sole dictator of your financial decisions. Consider the impact on your overall wealth, potential tax implications, retirement goals, and life circumstances.

If you’re interested in learning more, we very much encourage you to ask your CPA or schedule a free consultation with GenFi.