Maximizing Tax Deductions for Doctors: A Guide

With the advent of the always-certain tax season fully upon us, it’s worth remembering that, as some of the highest-earning professionals in the U.S., independent contractor physicians stand to save tens of thousands of dollars this time of year—or not.

But maximizing tax deductions for doctors is no straightforward task. Below, we’ll delve into the key deductions, provide practical examples, and share resources to aid in this critical aspect of financial management for healthcare professionals.

As always, remember that if you need advice specific to your situation, Core Clinical Partners has teamed up with a trusted partner and financial advisor in Generational Financial Partners, which specializes in working with physicians (95% of their client base). We encourage you to reach out directly to founding partner Ben Yin and to schedule a free, 30-minute consultation.

Understanding Tax Deductions: Basics for Doctors

Tax deductions can be pretty labyrinthine, so it’s important to understand the basics. A tax deduction reduces your taxable income, thereby lowering your tax liability. That means you’ll be taxed on less income than you earned, and may even shift you into a lower tax bracket.

That’s why it’s essential for doctors, particularly those who work as independent contractors, to understand what qualifies as a deductible expense.

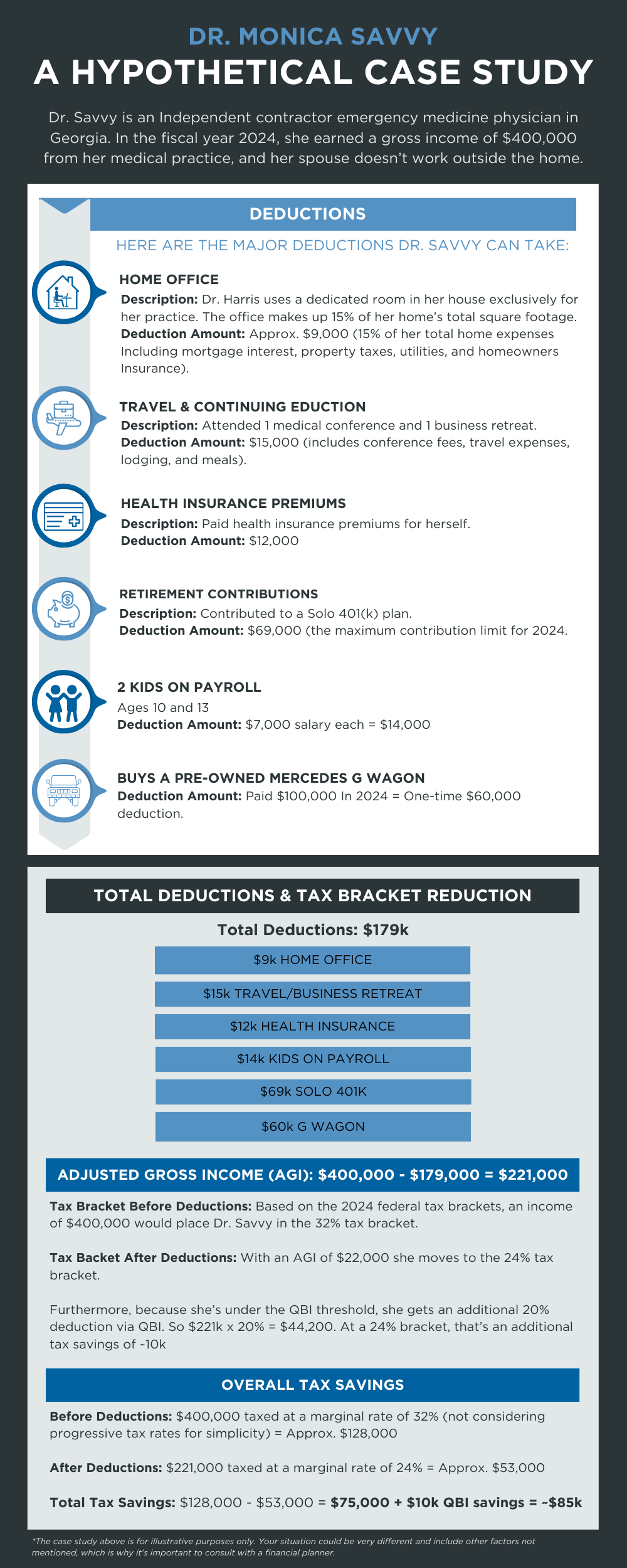

Common Deductions for IC Doctors

Independent contractor physicians have access to a broad range of tax deductions. Let’s explore some critical areas where physicians can maximize them:

- Home office expenses

- The IRS stipulates specific criteria to qualify for this deduction. The space used in your home must be designated exclusively and regularly for business purposes.

- For example, as a doctor, if you have a home office where you manage patient records or conduct telemedicine consultations, you can deduct a portion of your rent, mortgage interest, utilities, and insurance. The amount deductible is proportional to the size of your home office compared to the total square footage of your home, offering a significant avenue for tax savings.

- The Car Deduction

- Everyone is asking about this nowadays, and for good reason. Section 179 of the tax code allows you to deduct part of the purchase price of a vehicle as long as it has a “gross vehicle weight rating” (GVWR) above 6,000 pounds. Vehicles that qualify include the Mercedes G Wagon and the Tesla Model X. TaxFyle has a complete list of qualifying vehicles.

- In 2022, the law allowed for a 100% deduction in the year of purchase. For example, if a doctor purchased a Mercedes G Wagon in November 2022, even if it was financed, and even if it’s used (it just has to be “new to you”), they could take a 100% deduction of the vehicle’s cost—in the case of a G Wagon, that meant not paying taxes on around $150,000.

- Unfortunately, in 2023 the deduction percentage was reduced from 100% to 80%, and in 2024 it has been reduced further to 60%, though you can deduct the rest spread out over several years. Still, in this scenario, in year one, the same $150,000 vehicle would provide a $90,000 deduction in year one, equating to approximately $27,000 off your taxes, assuming a 30% tax rate.

- Medical supplies and equipment

- Any equipment or supplies that are directly used for patient care or the operation of your medical office qualify for this deduction. This can range from high-cost items like diagnostic tools to everyday necessities such as scrubs, stethoscopes, and even Hoka shoes.

- For independent contractor doctors, keeping a detailed account of these expenses can result in substantial tax benefits, as these are essential tools for their practice.

- Retreats, travel, and continuing education

- Expenses related to travel, continuing education, and corporate retreats can usually be deductible. This includes costs incurred while attending medical conferences, seminars, or traveling to various work locations.

- Meanwhile, the IRS generally recognizes the legitimacy of a business retreat for purposes such as planning your workload for the upcoming year, setting business goals, engaging in Continuing Medical Education (CME), or even strategizing to maximize Relative Value Units (RVUs). Such a retreat could last a week or ten days, and all related expenses can be deductible. This can include costs for accommodation, meals, travel, and any other necessary expenditures related to the retreat. Furthermore, if your spouse or children are legitimately employed by your practice, their expenses for the retreat could also be deductible.

- Insurance premiums

- Insurance premiums, particularly those related to professional liability, health, and business insurance, are fully deductible if they are used solely for business purposes.

- This deduction is particularly relevant for doctors who, given the nature of their profession, often benefit from extensive insurance coverage. By ensuring that these premiums are designated for business use, doctors can leverage this deduction to lower their taxable income.

- Note that most employers provide some form of medical malpractice coverage, so those are not among the types of expenses physicians normally deduct.

- Retirement contributions

- Contributions made to plans like SEP-IRA or Solo 401(k) can significantly reduce taxable income. For instance, a doctor who maximizes their contributions to a Solo 401(k) plan not only secures their financial future but also enjoys immediate tax relief. This strategy is especially beneficial for high-income doctors looking to reduce their tax liability while investing in their retirement.

- In 2024, you can contribute up to $69k/year (or $76.5k if you’re over 50) to a defined contribution plan such as a SEP IRA or a Solo 401k.

- Qualified Business Deduction

- One of the most advantageous tax breaks for doctors, especially those operating as independent contractors, is the Qualified Business Income (QBI) Deduction, commonly known as Section 199A deduction.

- The QBI allows eligible professionals to deduct up to 20% of their qualified business income from their taxable income. For example, if a doctor has $300,000 of net income from their private practice, they could potentially reduce their taxable income by $60,000 under this deduction.

- However, there are specific income thresholds and stipulations that must be met to qualify for this deduction. Sometimes physicians are over the income threshold ($383.9k/year if married and filing jointly), but if they utilize a defined contribution or defined benefit retirement plan, they can get under the threshold. Thus, it is imperative for doctors to consult with a financial advisor specializing in physicians to maximize this significant tax-saving opportunity.

- Social Security & Medicare Tax

- Unlike employed doctors, who share these tax responsibilities with their employers, independent contractors are responsible for the full amount, which totals 15.3% of their net earnings (12.4% for Social Security up to $169k of income in 2024 and 2.9% for Medicare). The silver lining here is that half of this tax (7.65%) is deductible when calculating their adjusted gross income. Therefore, while the burden is higher, the ability to deduct a portion of these taxes can provide a noteworthy reduction in overall tax liability.

- Pass-Through Entity Level Tax (PTE)

- In response to the $10k Salt limit, most states will allow IC physicians to pay some of their state income tax via their LLC (taxed as an S-corp) and enjoy a federal deduction. For example, if your LLC pays $15k on your behalf to the state of GA, your taxable income is reduced by $15k. Assuming a 24% tax bracket, that’s a savings of $3.6k.

Advanced Tax Strategies for High-Income Doctors

For doctors in higher tax brackets, certain advanced strategies can provide significant savings:

Kids on the Payroll

A very strategic yet often overlooked tax-saving strategy for doctors with their own practice is employing their children in the business. This approach not only provides a meaningful work experience for the children but also offers notable tax advantages.

Consider a scenario where a doctor employs their children to perform legitimate tasks like cleaning the office, handling paperwork, and filing. By paying each child a salary of $7,000 per year, several benefits arise:

- Tax Deduction for the Practice: The salary paid to the children is a deductible business expense, reducing the taxable income of the practice.

- No Income Tax for the Children: Since $7,000 is below the standard deduction for a single filer, the children do not owe any federal income tax on this money. This effectively transfers income from a higher tax bracket (the doctor’s) to a tax-free situation (the children’s).

- Opportunity for Roth IRA Contributions: With the children earning income, they become eligible to contribute to a Roth IRA. The $7,000 they earn can be fully invested in a Roth IRA, where it can grow tax-free.

This last benefit can turn out to have HUGE financial benefits for your kids. Consider this: if a 10-year-old starts putting away $7,000 each year for 10 years into a Roth IRA and then lets it grow for the next 45 years at a 7% annual rate of return, the total amount accumulated would be approximately $2.1 million. This amount would be available tax-free at retirement.

Employing children in your practice and utilizing a Roth IRA in this manner not only provides immediate tax advantages but also sets the foundation for substantial financial growth for your children’s future.

Professional Services & Investment-Related Deductions

Investments play a crucial role in the financial portfolio of many doctors, and associated expenses can be deductible. This includes CPA fees, financial planning fees, legal fees, and potentially other advisory fees.

Conclusion and Additional Resources

Navigating the complexities of tax deductions is crucial for doctors, particularly independent contractors. By understanding the available deductions, utilizing tools, and seeking professional advice, doctors can significantly reduce their tax liabilities. For further information, explore related articles on medical expense tracking, tax planning for doctors, and healthcare professional tax tips.

If you’re interested in learning more, we very much encourage you to ask your CPA or schedule a free consultation with GenFi.