At Core Clinical Partners, one of our core beliefs is that there is no one-size-fits-all way to organize a partnership with hospitals—and the same is true for our relationship with the physicians, nurses, and PAs who we hire to care for patients.

Whether you are employed and receiving a W-2 or are an independent contractor physician receiving a 1099 depends on a variety of factors including specialty and role. Most clinicians have been a W-2 employee at some point in their lives so inherently understand this model. The IC model is a little more foreign to many so it is important to understand the pros and cons of this tax status.

If you’ve recently gone from an employed model to being an independent contractor physician (ICP), or are starting your career as an independent contractor, you now face a bevy of often bewildering questions. One of the first is likely to be about the difference between forming an LLC and an S. Corp.

This is a complicated question that depends especially on which state you live in, as well as your personal financial goals and those of your family. To help our physicians navigate these choices, we’ve teamed up with a trusted partner and financial advisor in Benjamin Yin, founder of GenFi. Ben’s company specializes in working with physicians (95% of their client base) to build wealth and manage their financial goals. We definitely recommend consulting with a professional like Ben to come up with a plan that fits your particular situation and needs.

That said, let’s dive in.

What is the difference between an LLC and S Corp?

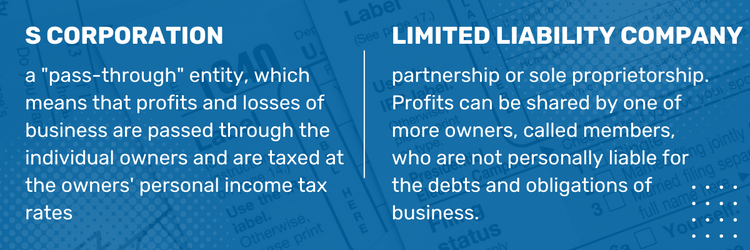

An S Corp, or S corporation, is a “pass-through” entity, which means that the profits and losses of the business are passed through to the individual owners and are taxed at the owners’ personal income tax rates.

Meanwhile, an LLC, or limited liability company, combines the benefits of a corporation with the flexibility and simplicity of a partnership or sole proprietorship. LLCs are also relatively easy to form and operate, and they offer some flexibility in terms of how they are taxed and how the profits and losses are shared. Those profits can be shared by one or more owners, called members, who are not personally liable for the debts and obligations of the business.

Contrary to popular belief, the purpose of an LLC for physicians is not primarily to shelter you from liability. The purpose is to help you save money by electing to be taxed as an S. Corp.

How does an LLC help lower your tax bill?

The best of both worlds: an LLC taxed as an S. Corp

Many independent contractor physicians choose to form an LLC for its simplicity and then elect to be taxed as an S-Corp for federal income tax purposes. This allows an IPC to enjoy the flexibility and simplicity of the LLC structure while also being taxed as a pass-through entity.

Here’s how it works:

- Physician creates an LLC (or a PLLC or a PC, depending on the State) taxed as an S-corp.

- The physician group, Core, for example, pays the LLC.

- The physician pays themself a W-2 salary (this salary is usually a lot lower than the overall LLC revenue but still needs to be “reasonable” per the IRS).

Remember, as an ICP, you are both the employer and the employee. Since self-employment tax (or, payroll tax) is only based on W-2 income, an independent contractor can often save thousands of dollars a year by taking a portion of income as a W-2 employee, and the rest as a corporate profit distribution. Note that this doesn’t help avoid income taxes— only payroll taxes. Still, these can add up to a lot of money for an ICP.

Self-employment tax is currently 15.3% (includes both employer and employee portions) on wages up to $160,200 (in 2023), and an additional 2.9% on anything above it—so coming in under that threshold on your W-2 could really help.

Here’s a quick example:

- Dr. Jones owns Jones Medical, LLC.

- Core pays Jones Medical, LLC $300k via 1099.

- Jones Medical, LLC pays Dr. Jones $100k via W-2.

- Dr. Jones’ payroll tax is now only based on the $100k of salary and not the entire $300k.

- Payroll tax implication without utilizing an LLC

- $160,200 x 15.3% = $24,510

- $139,800 x 2.9% = $4,054

- Total of $28,564

- Payroll tax implication utilizing an LLC

- $100,000 x 15.3% = $15,300

- Total of $15,300, a savings of $13,264

The next question is always, “what about the $200k that I’m not taking as wages?” That’s always your money that can be accessed via an owner distribution/withdrawal/dividend (can be transferred from your business bank account to your personal bank account with a click of a mouse). And the great news is, on that $200k, you don’t have to pay a single dime in payroll tax (remember, we’re not talking about income tax here).

Forming an LLC but getting taxed as an S Corp has a lot of benefits, but there are also some potential downsides, such as the requirement to comply with additional tax rules and regulations that apply to S-Corps. It is important for a physician considering this option to carefully weigh the potential benefits and drawbacks and consult with a tax professional before making a decision.

Whether or not it’s worth it usually comes down to personal goals as well as the particular regulations of the state in which you live and pay taxes. In general, if a state has no income tax (such as Tennessee), it may not be as worth it because these states usually add additional requirements, taxes, or fees for pass-through entities.

What is QBI and why does it matter?

In the past few years, the tax situation for independent contractors has only become more complex, meaning a lot of the information available online right now for independent contractor physicians is out of date. Again, it’s important to consult with a tax professional to discuss your particular circumstances.

That said, let’s start with qualified business income or QBI (i.e. Section 199A of the tax code). In brief, QBI refers to the net income or profit earned by a business that is eligible for certain tax deductions and other benefits under the Tax Cuts and Jobs Act of 2017. To be considered QBI, the income must be derived from a qualified trade or business—and to skip to the important part: income earned by physician independent contractors counts, BUT you have to make under a certain income:

- $364,200 (assuming married filing jointly in 2023).

- Above this limit, the benefits start phasing out until $464,200, at which point you won’t receive any benefit.

- QBI example:

- Dr. Jones makes $300k.

- After some expenses/deductions, their qualified business income is $250k.

- Receives a 20% QBI deduction based on the $250k. $250k x 20% = $50,000

- At a 25% tax rate, that reduces your federal tax bill by $12,500.

Avoiding the cap on SALT deductions

The same 2017 law that created QBI also put a cap of $10,000 on SALT deductions, or the ability to deduct “state and local taxes” from your income. The provision was aimed at reducing the tax deduction available for very high-income earners, such as physicians.

However, in response to that cap, many states have passed or proposed a so-called Pass-Through Entity (PTE) Level Tax. If your state allows PTE, you will be able to pay a portion of your state income tax via your LLC and take a federal deduction.

For example:

- Dr. Jones lives in Georgia.

- PTE-eligible state income tax liability is $12,000.

- Jones Medical, LLC pays the $12,000.

- At a 25% tax rate, that reduces your federal tax bill by $3,000.

Meet with your CPA

There is no doubt that organizing an LLC and then paying yourself as an employee of that LLC adds some complexity to your financial life. But doing so can potentially offer sizeable savings. In the examples above, Dr. Jones could save:

- $13,264 in payroll tax

- $12,500 QBI

- $3,000 PTE

- Total of $28,764

And this example doesn’t even account for savings as a result of retirement contributions or business deductions. The examples are simplified for illustrative purposes, and may or may not be applicable to your particular situation. Still, the potential upside is substantial.

If you’re interested in learning more, we very much encourage you to ask your CPA or schedule a free 30-minute session with Ben Yin at GenFi.

![]()