An LLC, or Limited Liability Company, separates a business’s assets and liabilities from those of its owner. But for physicians who are either newly entering the job market or who have spent their career until now as a W-2 employee, there can be several misconceptions and confusion about what the role of an LLC is and what it can (and can’t) do for you.

Core has teamed up with a trusted partner and financial advisor in GenFi, a company dedicated to helping physicians build wealth and manage their financial goals. We spoke to Nolan Pendleton, one of GenFi’s partners, about some of the misconceptions related to LLCs. Let’s start with probably the biggest one:

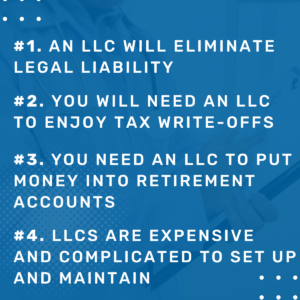

Myth #1: An LLC will eliminate legal liability

As the name suggests, most people understand the purpose of an LLC to be to limit liability. The idea is that if the business gets sued, the owner’s personal assets are protected from being seized to satisfy the debts of the business.

However, this protection doesn’t extend to the owner’s personal liabilities, such as those arising from their own professional malpractice. In the case of a doctor who sets up an LLC, if the doctor is sued for malpractice, their personal assets may still be at risk because they are the one providing the service and liable for their own actions. The “corporate veil” that separates the LLC from its owner can be pierced by a court, which means that the court can ignore the LLC and hold the owner personally responsible for any damages or debts. A court may choose to do this if it determines that the LLC was not operated as a separate entity, but rather as an extension of the shareholders’ personal affairs or if the corporation was used to perpetuate fraud or illegal activities.

So, while an LLC can provide some protection for certain types of business activities, it does not provide blanket protection from all legal liability, particularly in cases of professional malpractice, including medical malpractice. This is why it’s important for doctors to have malpractice insurance (with tail coverage!) in place to protect themselves from such risks.

All that said, it is precisely because of the risk of lawsuits that a doctor might consider putting other assets into an LLC, such as rental properties or large savings or stock accounts. Segregating these assets into their own company, and operating them as such, will provide additional protection to those assets if indeed a physician is targeted by a lawsuit during the course of their work as a doctor.

Meanwhile, an LLC can create a professional look, and there may be tax advantages and retirement plan contributions that can be made, but it is not a one-size-fits-all solution, and a CPA or financial advisor should be consulted to determine the best strategy.

Myth #2: You need an LLC to enjoy tax write-offs

This one is only a half-myth. When it comes to enjoying tax write-offs as a business owner, it is not necessary to have an LLC. You can still claim tax deductions through the IRS Schedule C form, which is the standard form used for business expenses. You would use that form whether you were a sole proprietor or an LLC.

However, having an LLC and filing as an S Corporation can give you additional tax benefits (we went into these in detail in our previous post, about LLCs vs. S Corps for physicians). In short, an LLC may allow you to write off above and beyond the typical limits for state and local tax deductions. This is an advantage that cannot be achieved through a Schedule C form alone. Whether or not you will want to do this will depend on your particular circumstances and goals, and which state you live in, so be sure to speak to your tax advisor or a CPA before making the determination.

Myth #3: You need an LLC to put money into retirement accounts

It is absolutely not necessary to have an LLC to contribute to retirement accounts. For physicians who are used to being a W-2 employee, they are likely already familiar with 401ks and other types of defined contribution accounts. The confusion comes in the mistaken belief that, as an independent contractor, you can only do an IRA or SEP IRA. In fact, an independent contractor physician could still decide to set up a 401k (or a defined benefit plan) for themselves regardless of whether they have an LLC—they just normally don’t because of the burdensome costs and paperwork involved.

The real benefit to having an LLC is flexibility in choosing how much of your LLC’s net revenue to take as income. For example, in order to max out a SEP IRA, net income from a Schedule C form would have to be $330k. But then you would pay more in payroll tax because that’s your self-employed income. Instead, if you set up an LLC and pay yourself less in income, you could save money in payroll tax but still max out a SEP IRA with lower amounts.

Myth #4: LLCs are expensive and complicated to set up and maintain

It depends on your definition of expensive and complicated!

Setting up and maintaining an LLC (Limited Liability Company) need not be difficult, or expensive. However, costs can vary depending on the state you live in and the requirements for record-keeping and annual filing fees. In total, the cost of setup and maintenance will come in around a few hundred dollars each year, which would be deductible.

Once formed, maintaining an LLC does require ongoing attention, such as keeping accurate financial records, filing annual reports, and complying with tax laws. While this may seem daunting, it is certainly less burdensome than maintaining a corporation. Meanwhile for a physician, forming an LLC can offer significant tax benefits by allowing for pass-through taxation, which means that the income generated by the LLC is passed through to the owners’ personal tax returns, potentially lowering the overall tax burden.

If you’re interested in learning more, we very much encourage you to ask your CPA or schedule a free 30-minute session with GenFi founder Ben Yin.